Photo by: Dept. of Finance

Homeowners in New York City accrue over $100 million in unpaid property taxes and water charges each year. A legal claim against the real property for these unpaid taxes and charges is called a lien. It is common practice for local governments to bundle and sell liens at deep discount to third party investors.

Lien sales make sense: Every dollar that governments do not collect from taxpayers is another dollar that has to be made up through future rate increases for everyone else, or by issuing more debt. Lien sales maximize tax revenue without tying up the limited resources of city government. But there is a dark side to the tactic.

Under current law, New York can sell a lien on a property if there is property tax debt of at least $1,000 that is three or more years overdue, or if there is water or sewer debt of at least $2,000 that is one year overdue. For the most part the current system works, due in large part to legislative reform last year championed by Brooklyn City Councilman Al Vann, along with the Neighborhood Economic Development Advocacy Project (NEDAP), the Legal Aid Society and Legal Services NYC.

The city recently collected over $80 million in back taxes after 90-day pre-lien sale notices were mailed citywide to over 22,000 homeowners. The city issues multiple warning notices imploring owners in arrears to make payment arrangements before liens are sold. Notice is given in multiple languages (e.g. Chinese, Korean, Russian and Spanish) where appropriate.

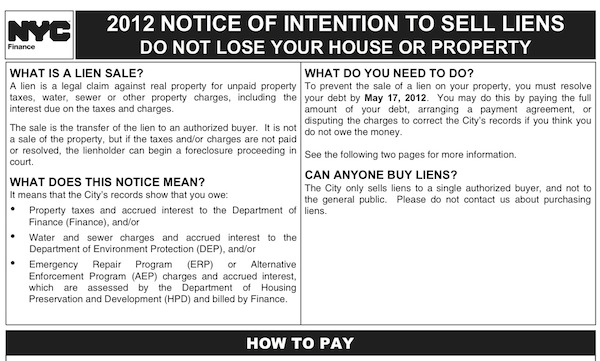

Payment plans for property taxes are made with the City’s Department of Finance (DOF); payment plans for water and sewer charges are made with the Department of Environmental Protection (DEP). This year an owner must make a payment plan on or before May 17th. The revised payment guidelines are generous, allowing for zero down-payment and terms of up to 10 years. Further, the new law provides clear guidelines that qualify our most vulnerable residents, particularly the elderly (65 and older) and the low-income (total combined family income below $37,400) for exemption. Veterans and military personnel on active duty are also exempt.

However, thousands of New York homeowners, many of whom no longer even carry a mortgage, could still lose their homes to foreclosure for unpaid taxes of a few thousand dollars – if they somehow failed to follow the guidelines described above.

Consider the case of Lana, an 82-year-old Latina resident of the Bronx who paid off her mortgage in 1977. She receives $710 per month in Social Security and rental income from a commercial unit on the ground floor of her 2-unit home. Lana fell behind on her water and property taxes after her tenant ran up a huge water bill and then moved out, leaving the commercial space in severe disrepair. Though she made a payment plan for property taxes, the city placed a lien on her home for water charges. By the time she learned of the water lien the city had already sold it to a private trust that buys liens in bulk, Xspand, a subsidiary of JPMorgan Chase. Though the original water charges were $15,193, within 15 months Xspand demanded total payment of $29,453, including add-on surcharges, interest and fees. As a senior citizen with limited income Lana should have been exempted from the lien sale. It is unclear how such cases deserving retroactive exemption will be treated.

The case of Lana is but one example of how a system with good intentions can too easily self-implode. A homeowner’s viable options are greatly reduced once the tax lien is sold, since surcharges, fees and higher interest rates can be levied by the lien purchaser. There are countless similar situations throughout the five boroughs. Simply legislating protection for the vulnerable and the underserved unfortunately doesn’t result in the protection they need. We must therefore increase the awareness level in our neighborhoods by spreading the word block by block and home by home to inform property owners that they must be proactive in controlling their financial destiny – and that they must take action before May 17th or forfeit their right to avoid a lien sale.

Toward this end the New York Mortgage Coalition recently awarded a $15,000 grant to the Coalition for the Improvement of Bedford Stuyvesant (CIBS ), a Brooklyn-based coalition of neighborhood nonprofits collaborating to address quality of life issues in Bed-Stuy. Through a systematic door-to-door campaign, directed and staffed by volunteers, CIBS is determined to reach every Bed-Stuy property owner potentially facing a tax lien. The CIBS campaign culminates with a Help Night on Wednesday May 2nd, when representatives from the city’s Departments of Finance, Environmental Protection, and Housing Preservation and Development will be on hand to answer questions and make payment arrangements. Help Night will take place from 5 pm to 8 pm at Bedford Stuyvesant Restoration Corporation, at 1368 Fulton Street in Brooklyn.

Legislation, regardless of how strong and well-conceived, is never the complete answer. We endorse the CIBS strategy of mobilizing community action through strategic, neighborhood-based activism.