“A detriment to building sufficient affordable housing is the long and laborious path projects must go through to reach completion.”

Ron L. Glassman

Filling in the “missing teeth,” like with the Madison Putnam infill project in Brooklyn.A detriment to building sufficient affordable housing is the long and laborious path projects must go through to reach completion. Projects built via the Low-Income Housing Tax Credit (LIHTC), a major source of affordable housing, have multiple sources of financing and long and complicated processing requirements. In New York City, from the time an application is accepted to a construction start, two to three years can elapse.

Add to that the building out of a project, followed by complicated rent up protocols, and the total process, from start to being fully leased and operational, can take six years or more. If a project requires rezoning and/or sites transferred from public to private ownership, the time period may be even longer, with no guarantee of success. Both Gov. Kathy Hochul’s housing initiative and Mayor Eric Adam’s BLAST plan are designed to improve the latter processes.

Pricing for projects over such long periods is fraught with uncertainty, leading to highly conservative cost estimating. This reverberates throughout the affordable housing industry characterized by ever higher development costs. Thus, the call for more public subsidies to off-set those higher costs, while production still falls behind the need. The result: too much subsidy going to too few projects.

Contrast this with the speed of gentrification in many low and moderate-income communities. A small army of builders and developers looking for the next “hot” neighborhood buy and build market rate housing in residentially-zoned areas, often outpacing affordable housing production. Projects are done “as of right” with the only subsidy, if used at all, the now expired 421-a real estate tax benefit program. Projects typically take two to three years to completion.

How can affordable housing be built with the same speed and agility as occurs in many gentrifying areas? Below is a plan, not presented as a substitute for rezonings or LIHTC, but as a supplement to create more housing for low and moderate-income households.

First, designate low and moderate-income communities that are residentially zoned for low and mid-rise apartment buildings (R-5, R-6 and R-7) that contain both vacant and underbuilt lots where new housing may be built.

Throughout the city, there are many available residentially zoned sites supported by existing infrastructure. NYU’s Furman Center reports that in R-5 and R-6 zoned neighborhoods there are over 38,000 vacant and underbuilt lots, predominantly 20 to 25 feet wide and 70-100 feet deep. The potential to build new apartments on these sites, as well as on R-7 zoned sites, could number in the tens of thousands.

These areas, in communities such as east and central Brooklyn, The Bronx and Upper Manhattan, can be designated to receive incentives to build affordable housing. This is akin to the designation of neighborhood preservation areas in the 1970s to preserve deteriorating apartment buildings.

Second, pre-approve replicable prototypes that can be built on commonly available sites in the designated areas. The city’s Department of Housing, Preservation and Development (HPD) can pre-approve designs and specifications for apartment buildings that can be built on available sites in the designated areas.

On the 20-25 foot R-6 sites, a small set of prototypes can be designed to contain between four and eight residential units, and on the R-5 sites, three to four units. These buildings can fill-in the “missing teeth on a block” or create stretches of row houses for contiguous sites (may be a role for factory-built models). A base price for prototype construction can be established, adjusted for site conditions and the scale of production. Further adjustments over time can be made for inflation and changing building regulatory requirements.

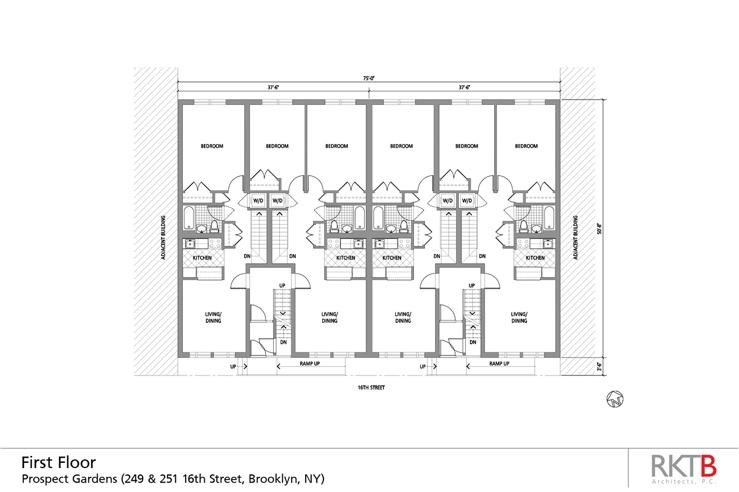

Above: First CPC R-6 Infill Prototype on 16th Street, Brooklyn, Completed in 2004.

Credit: John Bartelstone

Third, incentivize qualified for-profit and non-profit owner/builders to build these prototypes as affordable housing. The state and city should enact an “as-of-right” long-term (30 to 35 years) real estate tax abatement and exemption program, similar to the now expired 421-a program, specific to building the affordable prototypes.

This can be paired with the city’s long established subsidized financing program (the Participation Loan Program “PLP”) – combining market rate funds with 1 percent public funds to finance these developments. HPD and its partnering banks can establish pre-approved underwriting standards combining the subsidy programs with bank funding.

Fourth, develop an opportunistic funding mechanism that can act quickly to purchase sites when markets conditions are favorable. Today’s current high interest rates, and the absence of the city’s 421-a tax incentive program for new construction, has created a window of opportunity to purchase privately owned sites at relatively low prices compared to the past few years.

To take advantage of this, HPD can establish a price cap for site purchase, with the amount eligible for financing being the lesser of the cap or the appraised value of the site. The partnering bank would provide an acquisition loan timed to match a typical sales contract, e.g., closing 45 to 60 days after contract signing, subject to due diligence. To both incentivize the purchaser and confirm HPD’s commitment of the site’s eligibility for incentives, a 90 percent acquisition loan would be made, 60 to 65 percent with a first mortgage from the partner lender, with the balance up to 90 percent provided by a 1 percent second mortgage from HPD.

Is it less expensive to buy private land for affordable housing than to wait for the disposition of low-cost public land? Given the time for such dispositions (often measured in years) and the uncertainty of success, the answer is yes, particularly when economic conditions depress the price of land. The affordable housing community needs an institution that can spring into action to take advantage of market opportunities.

The Community Preservation Corporation (CPC) was such an institution during the market downturn in the early 1990s when it financed the renovation of dozens of defaulted Freddie Mac financed apartment buildings. The savings from Freddie’s discount of their defaulted mortgages enabled the affordable renovation of dozens of apartment buildings using little or no direct public subsidy other than the City’s now expired real estate tax incentive program for upgrading existing buildings (J-51).

A further example was the distressed sale to CPC of the Helmsley’s organization 6,362 apartments and commercial interests at Parkchester for $4 million. This enabled the massive affordable upgrade of Parkchester’s 12,271 apartments between 1998 and 2005 with no direct public subsidy other than an expanded version of J-51 real estate tax benefits. The default of Signature Bank may present similar opportunities for its mortgaged residential properties in need of repair.

Fifth, pre-approve underwriting standards to support the cost of building and operating the affordable prototypes: balancing affordable rents, long-term financial health, with adequate returns to incentivize development.

Model standards might include:

- HPD can establish affordable rents for income qualified residents, subject to rent stabilization for 30 years, assuming the regulatory system fairly passes along inflationary costs of operation.

- Items to be financed include site acquisition as described above; construction cost of prototype (adjusted for unusual site conditions and/or the scale of production and typical soft costs) Financing up to 90 percent of eligible costs to be provided.

- Operating expenses adhere to HPD standards, including long-term real estate tax abatement and exemption. Debt service would be a mix of market rate and subsidized financing to achieve a sufficient cushion (debt service coverage) for the sound management and operation of the apartment building.

The above underwriting can incentivize prototype development. The program’s high level of financing, low market risk for renting and potential growth in cash flow, given long-term fixed-rate financing (see below) and long-term real estate tax abatement, can provide for long-term healthy and stable investment returns. It might also provide an attractive alternative to building market rate housing in gentrifying communities, thus moderating gentrification’s effects and possibly achieving a more stable, economically integrated community.

Curtis+Ginsberg Architects, photo by John Bartelstone

Homes on Malta Street, Brooklyn, an example of using prototypes in contiguous sites.

Sixth, project financing involves first mortgage funds from a private lender, with a percent second mortgage from HPD. Subject to their mutual approvals, the HPD partner-bank(s) would provide the construction loan for the project, with HPD providing a 1 percent second mortgage. The bank would vet the experience and financial strength of the builder/owner, requiring necessary completion and financial guarantees. The city would deposit all subsidized funds with the lender, to be advanced as construction progresses. A single engineer/architect, under contract with the lender, would represent both the city and lender, and approve all construction advances and change orders consistent with pre-approved construction loan agreements.

Seventh, long term financing can be provided by the New York City and New York State public employee pension funds. Created in 1983, the New York City pension funds launched a program that can provide a forward committed (two years or longer) long-term (up to 30 years) fixed-rate mortgage (priced off market indices) that provides a take out for the construction loan. This forward commitment protects affordable projects from spikes in interest rates. It is credit enhanced by either the State Mortgage Insurance Fund, or by the city insurance program for 100 percent of its original mortgage principal. The insurance becomes effective once the property stabilizes, with all public subsidies in place. The pension fund then purchases the construction loan of the lender bank at par at the forward committed interest rate.

Documentation for the transactions are all pre-approved, resulting in minimal closing costs. This process has frayed in the past decade, due to difficulties in coordinating municipal sign-offs, and additional processing requirements of the pension funds. The latter can be remedied with the fund’s recommitment to the investment program’s original intent.

Eighth, inherent in the plan are many “fast track” processes, which can save time, money, and make the program accessible to a broad spectrum of owner/developers.

First, fast acquisitions can occur of private land compared to lengthy transfers (often a year of more) of public land to private for profit or non-profit ownership. Second, pre-approved prototypes can narrow the scope of reviews by HPD, significantly shortening the processing time by possibly a year or more. Additional time may be saved by the Department of Buildings dedicating a unit to assure consistent and expedited plan reviews. Third, HPD is working to quicken the rent-up process so it can be more closely timed with the completion of construction, thus minimizing carrying costs.

Much of the processing for the pre-development phase can be done by the partner banks, in accordance with pre-approved standards. This can leverage the use of HPD staff as their functions shift from their involvement in the details of individual transactions, to oversight of their banking partners’ adherence to program standards.

Significant savings of time and money may be realized. Based on past efforts, combining the efficiencies noted above, this plan may save up to two years to produce and tenant the prototypes compared to typical LIHTC projects. This should also reduce the overall development costs and, depending on the level of desired affordability, lower the amount of direct public subsidy required.

On what basis can we surmise this? The antecedent of this approach is the “vacant building” program initiated under Mayor Ed Koch and continued by the Dinkins administration. That program rebuilt thousands of vacant, city-owned buildings that were abandoned in the the 1970’s. Other than the acquisition price (buildings cost $1 each), major development terms were essentially pre-approved—design, subsidies, underwriting, financing documentation, construction administration and rent-up procedures.

The Community Preservation Corporation, the primary HPD partner in the program, financed over 15,000 apartments with development costs averaging about $75-$85 thousand per apartment, up to half as much as other approaches used to rebuild the city’s vacant buildings. Processing time from application to construction closing was approximately six to nine months, with construction and occupancy about two and a half to three years later.

CPC tried a variation of this approach in the early 2000s when it worked with RKTB Architects to create a prototype for in-fill housing for R-6 zoned areas. Fifty-plus, 8-unit four-story walkup buildings were constructed on vacant privately owned sites between 2002 and 2010. Construction costs ranged from $120 per buildable foot for the first buildings, to about $180 a foot for the last property completed in 2012.

Ronald L. Glassman/RKTB

The Msgr. Anthony J. Barretta Apartments in Brooklyn (formerly known as Our Lady of Loreto).

Effective implementation of the proposed program will require leadership from Mayor Adam’s office, as occurred during the Koch/Dinkins era “vacant building“ program. As this program matures, one might envision it becoming institutionalized as one of the primary tools to meet the City’s diverse affordable housing needs. Contractors and other professionals specializing in building various prototypes, might bring other efficiencies to its development.

Variations of this program might be adapted for home ownership.

Michael Lappin is the former CEO of the Community Preservation Corporation (1980-2011) and currently founding member of Lappin Associates, a provider of advisory services for affordable housing. During his tenure, CPC financed and developed over 90,000 affordable apartments in New York City.

One thought on “Opinion: Bringing Affordable Housing to NY’s Market More Quickly, and Less Expensively”

wow, thats one of the best strategies, that real affordable housing can move forward with, but now here is the big question, will the mayor adams who receives big money donations from some shady big time developers who only interested in building high end market rate aparmtments, will he are governor kathy another behind closed doors dealer, move on this idea? seems to me and others, not, high end rental buildings going up fast, in gentrifying neighborhoods, and going up in segregated well of to do areas, maybe now when they say WE LOVE NY, it means they love the big time real estate developers, not the small time tax paying joe are jane