Robin Hood Foundation

A key chart from the new Robin Hood 'Poverty Tracker' report.

It’s common to blame poverty on life’s deep wiring, like a person’s lack of education or the racial discrimination they have faced or their immigration status. Poverty is explained as the product of a reaction between societal structure and the personal characteristics that a low-income individual cannot quickly change, if they can change it at all.

A report out today from the Robin Hood Foundation indicates, however, that poverty is a much more fluid phenomenon than more-comfortable New Yorkers might realize. In the fourth of its quarterly “poverty tracker” reports, the foundation finds that 47 percent of New Yorkers were in poverty at some point over the 2012-2014 period, but 5 percent were living below the poverty line for that entire period. (It’s tempting to say only5 percent; the number, however, represents 400,000 people.)

Among those 47 percent are likely some New Yorkers who encountered poverty as part of their income life-cycle: In other words, they arrived in the city as a person living in poverty but now, having finished college or gotten their business off the ground, they are on track to have a more comfortable life. Some other part of the 47 percent, however, represent people who cycle in and out of poverty — and therefore, even if they aren’t among the million or so New Yorkers considered “poor” at any moment in time, they are often on the precipice.

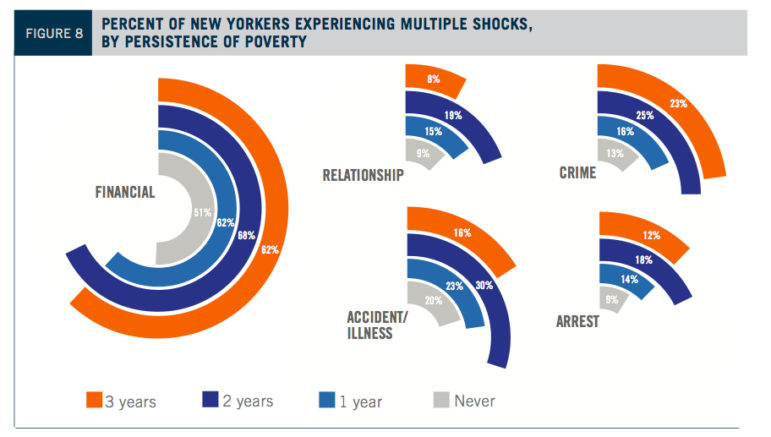

One question the authors of the report (Christopher Wimer, Sophie Collyer, Irwin Garfinkel, Matthew Maury, Kathryn Neckerman, Julien Teitler and Jane Waldfogel) had was the relationship between finding oneself in poverty, severe material hardship or poor health and experiencing a sudden life emergency, or “shock” as the writers put it. They focused on five types of shock: a sudden financial hit for lost income or unexpected expense, the end of a romantic relationship, suffering an accident or illness, being the victim of a crime or being stopped or arrested by the police.

What they found is an interesting relationship between shocks and the persistence of poverty.

Across the board, the population most affected by shocks was the group of New Yorkers who reported poverty in two of the three years the survey’s been going (the tracker follows the same households over time).

And those who were poor for only one year out of the three were more likely than those who were poor for the entire three-year period to have suffered from an arrest, an illness or relationship trouble—and the two groups were equally likely to have suffered a sudden financial emergency.

What emerges is perhaps a tale of two poor cities: One persistently living below the poverty line and the other moving in or out of poverty because of sudden changes in fortune. But, as the author notes, another explanation is just as valid: Those households suffering shocks because they had become poor.

In fact, it could be a little of both. The authors used a statistical modeling technique and found that the numbers support “the notion that causality runs in both directions.”

“In other words, multiple shocks at one point in time increase the likelihood of subsequent hardship, and hardship at any point in time leads to a higher probability of more shocks later,” the report concludes. “This notion makes intuitive sense and suggests that protecting families from repeated exposure to multiple shocks can help prevent severe and persistent hardship.”

Another conclusion that is clear from the chart above: Life emergencies like illness, arrest, crime or divorce play a role. But, not shockingly, income is what is most associated with spells of poverty. That’s an important consideration for policymakers deciding whether to focus on safety-net programs or on non-monetary ways of helping low-income New York.

One thought on “Researchers Ask: Do Life Crises Create Poverty, or Vice Versa?”

Interesting research that leaves me with two initial questions:

1. Did they look at wealth or just income? I would think wealth, especially family wealth, is a stronger predictor of outcomes.

2. What about various forms of displacement as a shock? I’m thinking about the research on eviction, as well as the larger theory of Root Shock and serial displacement from Dr. Mindy Fullilove.