Photo by: CNYCN

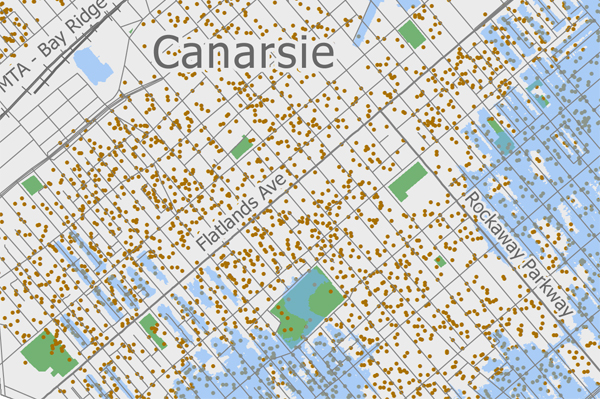

A map prepared by the Center for New York City Neighborhoods. the dots are households that, over the past three years, have received pre-foreclosure notices. The blue shows the reach of Sandy floodwaters.

Four years after the city’s mortgage delinquencies hit their peak, homeowners’ advocacy groups fear a new foreclosure crisis looms in neighborhoods devastated by Hurricane Sandy. In recent weeks they have sounded the loudest alarm for Canarsie, on Brooklyn’s southeastern shore, where floodwaters from Jamaica Bay swamped a district already struggling with some of the highest foreclosure rates in the city.

“Canarsie is one of those places where it’s just storm upon storm,” says Marilyn Gelber, president of the Brooklyn Community Foundation, which is moving to allocate some of its $2 million Sandy recovery fund to help develop a homeowners’ assistance program in the neighborhood. “It is a community in jeopardy.”

The city’s flood zones in Brooklyn, Queens and Staten Island contained thousands of households that were already behind on mortgage payments when the October storm ravaged their properties. Nearly four months later, those and other homeowners are still scrambling for funds to cover repairs, lost rental income and alternate housing. Soon after the storm, nearly all banks granted homeowners temporary suspensions of mortgage payments for 90 to 180 days, but as those moratoria end, many homeowners will be unlikely to come up with the large lump sums—totaling four or seven months of payments—that will be due, advocates say.

Legacy of predatory lending

A historically working-class area with about 200,000 residents, Canarsie contains one of the largest concentrations of one- and two-family houses in the city: 58 percent of households own their own homes—the highest home ownership rate in Brooklyn, according to 2011 data from the Furman Center for Real Estate and Urban Policy at New York University. The neighborhood also has the second-lowest poverty rate in Brooklyn.

But Canarsie’s residents, once mostly Jewish and Italian but since the 1990s largely black and Caribbean, were targets of predatory lending during the housing boom—given adjustable-rate mortgages they could not afford once interest rates spiked from two to nine and thirteen percent, says Tonya Ores, executive director of Neighborhood Housing Services of East Flatbush (NHSEF). In early February the non-profit hired a community outreach coordinator to focus solely on Canarsie, and the agency is planning three meetings in March to help homeowners fend off anticipated mortgage troubles.

One challenge for Canarsie is that no strong homeowners’ groups currently exist, Gelber notes. But to cope with storm recovery and mortgage woes, a coalition of groups, led by Deputy Brooklyn Borough President Sandra Chapman, herself a Canarsie resident, has formed the Canarsie Recovery Center in recent weeks to assist homeowners in preventing a big new foreclosure crisis.

Given the concentration of subprime loans in Canarsie from 2004 to 2007, it’s no surprise the neighborhood now has high a high rate of delinquent mortgages, notes “Homes Underwater: Forbearance Alternatives for Sandy Homeowners,” a recent white paper from Queens Legal Services. In 2011, nearly 3,000 households in Canarsie received pre-foreclosure notices, the highest of any New York City neighborhood, according to that report. More than half of those homes were located in Canarsie’s flood zone; based on the latest FEMA-Sandy flood boundary, 1,704 households in the disaster area received notices between February 2010 and January 2013 indicating they were 90 days or more behind on their mortgage payments, according to data from the Center for New York City Neighborhoods (CNYCN), a non-profit formed to respond to the mortgage crisis.

Scars from Sandy are visible

On block after block of the district’s flatlands—former marsh surrounded on three sides by water—signs of storm damage and ongoing repairs are evident. Tidy stacks of ruined carpet, warped floorboards and water-logged insulation still line the curbsides, and sandwich boards heralding contractors at work dot front lawns. Homeowners like Luesta Haggie on Seaview Avenue faced waist-high floodwaters that swept along from house to house, filling her basement and ruining her car, while others, like Lenore Katz, of Flatlands 10th Street, found their basements destroyed when sewerage drains backed up into their homes.

But while the damage from the storm is visible, knowing how many and which Canarsie homeowners face an imminent foreclosure threat is more difficult.

Lenders offered homeowners in declared disaster areas a 90-day break from mortgage payments, a period that expired at the end of January. Wells Fargo, for example, granted 90 day suspensions on its own loans, and followed suit on loans it services for Fannie Mae and Freddy Mac when the federal Department of Housing and Urban Development announced an extension of its moratorium until late April, according to Marie Day Hayes, senior vice president responsible for the bank’s northeast community outreach. NHS’s Ores says most lenders in Canarsie extended the moratoria for another 90 days, making payments due around May 1st, depending on the lender.

Thus, it’s too early to report numbers of new foreclosures. But since the storm, many more households are likely struggling with their mortgages, says CNYCN’s executive director, Christie Peale.

“Right now the data is not captured in the usual sources,” Peale says. “More than anything, we’re worried about the people we don’t know about.”

To that end, Rudolph Chase, the community outreach coordinator hired by NHSEF, on Saturday led a group of volunteers who canvassed the neighborhood to survey residents’ needs. Chase said he is still collating the results of questionnaires, but “overall, the consensus is the storm really took a toll on the community,” with many homes still awaiting repairs. “It looks like we are still far off from a recovery.” He does not yet have a clear picture of how the forbearance period and foreclosure threat is unfolding, he said, but plans additional canvassing in the coming weeks.

But anecdotes provided by clients of the groups behind the “Homes Underwater” white paper suggest that some homeowners in other neighborhoods have had difficulty getting lenders to agree to forbearance extensions, loan modifications or affordable payment plans. Some homeowners reported being charged late fees, denied any forbearance period, and receiving notice of foreclosure action a month or two after the storm.

Grace period could help, or hurt

Indeed, banks and homeowners’ advocates alike warn that post-disaster forbearance periods can be more harmful than helpful when they require full payment at the end of the moratoria. After Hurricane Katrina, New Orleans experienced a foreclosure boom when forbearance periods ended, Peale notes. The groups behind “Homes Underwater” have called for a one-time, twelve-month waiver of principal and interest payments due for residential mortgage loans secured by homes directly affected by Hurricane Sandy; barring that measure they suggest banks forbear payments and suspend interest for twelve months.

The white paper also calls for banks and lenders to adhere to a uniform policy regarding forbearances, which have so far varied from bank to bank, which could be publicized to help homeowners plan for future payments. Day Hayes, of Wells Fargo, said its customers should contact the bank to discuss their circumstances and that the bank would work with customers on a case-by-case basis to consider additional forbearance or, in the case of delinquencies, loan modifications. “We work with the goal of getting them to an affordable payment,” she said. In cases where the bank has not yet had contact with customers, forbearance is being automatically extended until April 26, she said.

Ores says that while a few homeowners have contacted NHS for help with their mortgages because they depended upon rental income from units destroyed by the flooding, nearly all the one hundred or so calls it has fielded have been for help with paying for repairs or handling insurance or FEMA claims. So far, Ores says, no one has asked for help to handle the upcoming balloon payments or to avoid possible foreclosure when the moratoria end.

“People have really been focused on repairs,” concurs CNYCN’s Peale. “We’re encouraging them not to forget their mortgages.”

With over 32,000 city homes currently in the legal process for foreclosure, she says, “We’re desperate to avoid another wave.”

One thought on “Canarsie Braces for Foreclosure Wave After Sandy”

Pingback: Canarsie Home Rentals - My holiday places advice